Show Transcript:

The Big Idea

Finances don’t have to be scary

Questions I Answer

- What’s the best way to organize paperwork and bills?

- How can I automate my finances?

- What are some tips for saving money?

- What tools can I use to help make organizing my money easier?

Actions to Take

- I understand that managing finances can be scary. It can be daunting and really overwhelming. But using some automation, setting up some good habits can help you stay on top of paying your bills, tracking your expenses and avoiding late fees, which is where a lot of us really get hit hard.

Key Topics in the Show

-

How to best sort and organize paperwork

-

Using smart techniques to automate and simplify financial responsibilities

-

Creating systems that make saving simple and pain-free

-

Tools for avoiding the Diderot effect as income increases

-

Strategies to downsizing your debt

Welcome to season nine of Productivity Paradox with Tanya Dalton, a podcast focused on using productivity, not just to do more, but to achieve what’s most important to you. Join Tanya has she kicks off the New Year with a special season titled, New Year True You. And now here’s your host Tanya Dalton.

Hello, hello, everyone. Welcome to Productivity Paradox. I’m your host, Tanya Dalton and this is Episode 112, Finding Financial Freedom.

Today, we’re going to be piggybacking a little bit off of last week’s how to organize anything episode. And we’ll be talking about ways that you can organize and declutter your finances, your bills, and your expenses. I’ll also be talking about finding systems to help you save, and how automations can help you make that even easier.

We’ll discuss some strategies to dig your way out of debt, and how to be careful of the Diderot effect. But first, I want to say a quick word about today’s sponsor. If you’re looking for a simple way to create custom invoices, track expenses and get paid quicker by clients, check out FreshBooks.

This cloud based accounting software will help you streamline your business finances. And for a limited time, FreshBooks is offering a free 30-day unrestricted trial for my listeners. I’ll be sharing some more details about that a little later on in the episode, but let’s go ahead and dive into our topic for today.

I want to talk about how we can be more productive when it comes to our finances. How do we organize that mountain of paperwork that’s sitting on your desks? Because one thing that I hear again and again, over and over with so many people is that, they do have these piles of paper sitting there and they find themselves well, overwhelmed. They don’t really know what to do with it all, and it doesn’t help that most people don’t find this to be a particularly fun task.

No one really wants to go through mountains of mail, and bills, and invoices, and expenses, and magazines, and everything else that ends up in our mailbox each day. These piles end up getting pushed aside day after day, and these piles tend to grow,

and grow and grow until suddenly, there’s this tower of paperwork to go through. And then it’s an even bigger and more daunting task to conquer.

So, if you have a Mount Everest of paperwork to sort through, I suggest, let’s start there. Let’s dig into that first, and get that paper mountain decluttered and organized. And then when that feels more manageable, you can move on to setting up future habits, and automation in order to make that mountain into a molehill.

©Productivity Paradox Page 1 of 8

Now, when it comes to organizing paperwork, this is exactly the same as if you were organizing your bedroom or your kitchen. You can use that same methodology that I talked about last week with the four steps of prep, sort, purge and organize. And I want to remind you, just like we talked about last week, it doesn’t all have to be tackled at the same time. You can break this down and make it into a bite sized piece, work on it for like 15 minutes a day and you’ll start to make some really good progress without really overwhelming yourself.

Now, the only difference between what we talked about last week, and what we’re talking about today with our finances is with our three bins. Instead of having trash, keep and donate bins, you’re going to need to have three different bins. Because the last time I checked, charities do not accept donations of bills. It sure would be nice if somebody else would take those off my hands, but nobody else will.

So instead, you’re going to have a trash, file and shred bin. So, when you have those three bins ready, you’re ready to start tackling the paperwork. So, as you’re going through, I want you to look at the items that need to be thrown away, and toss them into that trash or rather, recycling bin, because most of our bills can be recycled. But if there are things that are private, you want to make sure and shred them.

And here’s my rule of thumb. If you have any questions, if you have any doubt about whether something should or should not be shredded. I say, shred it. Get rid of it. Take five seconds. Do that extra step of putting it through the shredder just as a little extra

security. So, anything that has your account number on it, especially if it has your social security number, I recommend shredding it.

The rest of your items, well, they’ll need to be filed away. So, that goes back to that whole philosophy of everything has a home. We want to make sure we’re not mixing up big piles of paper. So, bills should not be mixed in with invoices, which are mixed in with expenses or non related things.

So, I want you to remember, as you’re sorting things into that file bin, you want to put similar items together so that, when you’re ready to go into that last step where you’re organizing them and putting them in their place, you have all of your medical items together. Or you have all of your travel expenses together in a pile and so on. You can use accordion folders or file cabinets to sort, and organize those documents you want to keep.

Now, if you watched my Tanya TV episode last week, where I talked about how I organize my kitchen, you heard me talk about zones, and I think zones work really well here as well. It’s basically grouping things together that have a commonality. So for example, you could have a kid zone for all things related to your kids. Or maybe you have a car zone with paperwork related to your car. So things like insurance, car payments, receipts for your oil changes, and your mileage checkups and those kinds of things. That way, when it’s time to sell your car, you have all that paperwork together ready to go. No need to dig it back out.

What I want you to do, though, is I want you to figure out what grouping works for you. Does it work for you to have kids all together with all kid items? Or do you prefer

©Productivity Paradox Page 2 of 8

to have it divided into kids health, kids activities, and so on? So again, it’s this whole idea of figuring out what works for you to keep items together.

This going through the paperwork, it’s a pain. I’m not gonna lie, but it’s not really rocket science. It’s not really that difficult. It’s just a matter of rolling up our sleeves and getting it done. Because then once that’s completed, we can begin to figure out how to organize your finances. So once we have that mountain conquered, we’re going to move on so we can avoid this paperwork beast in the future.

I want to share with you three very simple, very easy tricks that I like to do on a continual basis to keep my finances organized. The first one, really easy sort your mail every day. Instead of allowing it to pile up and turn into that mountain, I recommend sorting through your snail mail every day. As you pick it up from the mailbox on the way to the front door, just do a sort. It literally takes 15 seconds to pull out the bills, put the catalogs in a pile and move on.

Because immediately what I do, is I take my bills and I put them in a to be paid basket. That way, you only have to pull out the things you need that needs your immediate attention as opposed to having one get wedged inside one of those 20 pound Restoration Hardware magazines, and then it gets lost and forgotten. We want to make sure everything stays together and it’s really simple when we’re ready to pay our bills.

The second thing is, have a dedicated email address for bills. I literally have a special email address that I don’t use for anything else except for my electronic bills. And I had it set up so that anything that’s sent to that special email address gets forwarded to my main email account, and gets automatically sorted into a folder called, bills to pay.

Now you could name your folder, anything you want. You can name it bills, finances, I hate bills, whatever you want to call it. What matters is, you’re automatically filing it without having to think about it. You’re streamlining and making it possible for your

electronic bills to be in one place, just like you do when you’re sorting your paper bills, and putting them into that to be paid basket.

Now, if you don’t want to have a special email address, that’s okay. You can still have your email sorted by using smart mailboxes, or having a special folder within your email program.

Most email programs will allow you to have a separate alias address that’s under your current email address, and you can filter it straight into that same inbox and into that folder you created. To me, this is one of the simplest things I can do, because it makes sure that all of my bills are together.

The third thing I do is, pay bills on a regular or a consistent day. I find that it’s helpful to have a consistent day where I set aside time to work on bills and finances. For me, this is Friday mornings. I call it financial Fridays.

You might remember back in Episode 35, and we talked about automation or like the theme certain days. This is one of those days. I set aside 45 minutes or maybe an hour

©Productivity Paradox Page 3 of 8

each week to go into my email folder that I just talked about, and I gather my to be paid basket, and I spend a batched amount of time paying all the bills that I have accrued at that time.

This way, it takes no time at all, and it streamlines the process. And since Friday is my dedicated financial day, I do all my budgeting and financing type tasks in that one day. That way, I’m not ever really stressing about it. I know it’s going to get done on Friday.

Now, I personally chose Friday because it makes me feel like I ended my week with a really big win. But if paying your bills before the weekend is a buzz kill for you, pick a different day. My sister likes to do it on Sundays, because then, she starts the following week knowing she’s put her bills behind her.

I have another friend who picks the 10th and the 20th of each month. So, she has enough time to get bills paid before the first of the month or by mid month. Ultimately, it’s up to you. Just make it a regular habit and put it on your calendar. Let’s stop thinking about bills and let it just happen automatically. And that’s what I mean when I talk about automated systems.

You’ve heard me talk about automated systems before. And when it comes to staying on top of your finances, one thing that can be incredibly helpful is using these automations that are already built into your banking systems. You know how much I love good habits in our daily routines. That’s because we don’t just think about it. We just do them. It becomes second nature, and it doesn’t require any thoughts like brushing your teeth.

In the world of finance, automations can work the same way. They can help create an automatic tasks that happens without us having to think about. So, there’s things like automatic withdrawals.

One example of an automated system would be that, if you had money automatically pulled from your paycheck and put into your 401(k), or some other savings or investment account before the paycheck even hits your bank account. That makes saving so painless. Rolling money into an alternate savings area before you have time to think about it helps you make sure you’re budgeting, and saving on a regular basis. You can also use automatic payments.

Another example of something your bank can do for you is, if you use an online banking program, they have recurring payment options. So, for example, if your rent or your mortgage are the same amount each month, you can set up a recurring payment and never have to worry about paying that bill each month. It’s done automatically.

This doesn’t work for things like your gas bill, which varies from month to month. But for the ones that are consistent, it definitely takes the thinking out of it. The only thing you need to be careful of is making sure you have sufficient funds to cover your payments, which brings me to automatic reminders.

That’s the great thing. Most banks have it set up so you can get an automatic notification if your bank account drops below a certain level. You can get an alert

©Productivity Paradox Page 4 of 8

when your funds dip below that amount that you set. Or you can get an alert on online banking payments if a payment has been made within a certain timeframe.

So, it’s really good to use these to our advantage. And these are things the banks already have set up and it takes no time at all to get working for you. This is the thing, getting our money to really work for us doesn’t really need to be difficult, and it doesn’t have to be hard to save money. That’s what I want to talk about next. But first, let’s take a quick word from today’s sponsor.

FreshBooks is a cloud-based accounting and invoicing software that can help you streamline your business finances. It allows you to customize invoices that can be sent to your clients with just a few simple clicks right from your desktop or even from their

mobile app. You can also set up automated reminders when clients are late paying invoices. Plus, with FreshBooks payments, clients can pay directly from your invoice, which means you get paid quicker. It doesn’t get any better than that.

So, join the millions of small businesses who are using FreshBooks, and you can try it for free for 30 days by going to FreshBooks.com/paradox. In the section that says, how did you hear about us? Just type in Productivity Paradox.

Okay, I want to talk about creating some systems for saving money, because I truly believe saving money doesn’t have to be quite so painful. For some of us, saving money is easy. And for some of us, it’s really hard. Some people are just natural savers and some are spenders. One of my nieces is going to be a saver. She gets candy at Christmas and somehow, it lasts through all the way through the following summer. Her sister, however, she’s the spender. She’s lucky if that bag of candy makes it all the way to New Year’s.

We all have differences, and it’s no different with our money. So, we have to exercise a little more will and control when it comes to saving for some of us, especially because there really is no immediate gratification when we’re trying to save money.

Saving money is one of those future planning things, and sometimes it feels better to spend money in the moment, right? So let’s piggyback off that idea of those automations we just talked about, because it’s a great way to save money without thinking twice about it. It takes the pain out of saving.

In fact, my biggest and my best tip on saving is to have money pulled out for investing before you get your paycheck. Set it up for an automatic draw and it makes saving painless because it happens without you even thinking twice about it. So before you can get that paycheck, it’s already gone and into that investment, that 401(k), or into your travel saving funds, whatever it is you want to do. You can even siphon it off to multiple different accounts if you want but that is by far, my favorite.

The second thing you can do is, live on an income. I know that sounds a lot easier said than done. But one thing you can consider is living off one income if you’re a two income family. When John and I got married, we always lived off of one income. We saved one person’s paycheck and we lived off the others, and that’s actually why we were able to survive on a teacher salary.

©Productivity Paradox Page 5 of 8

When John went back to school to get his MBA, we lived off my teacher salary. We had a baby and were all living off that teacher salary. But living on one paycheck, and saving other really can help you build up an amazing nest egg of savings. That’s honestly one of the ways that we were able to put money into our business and grow it, because we still do this today. We do not use both of our salaries. We live off of one and we save the other.

The third thing you can do is, when you get a raise, raise your savings. Anytime you get a raise, try to increase the amount that you’re saving and investing. Try to take half of whatever the raise increases, and put that automatically towards saving. Because you’ve been used to living off of your old paycheck, saving this amount, this half of the difference really will feel painless, because you’re still getting an increase, but you’re saving at the same time and that makes saving so much easier.

So, let’s talk about raises just for a second, because believe it or not, there can be some pitfalls when we get a raise. We have to be careful not to live up to our new payroll amount. We tend to want to acclimate to a nicer lifestyle as our paycheck increases, and that’s okay. We just want to be mindful about it.

We want to feel like we’re making more money so then we end up, a lot of times, spending more money and there’s nothing wrong at all with wanting to live nicer, or to have nicer things. It’s okay to live just a little bit nicer. You don’t have to go out and buy a yacht.

I mean, that sounds really nice, but we really want to keep our spending in check and not live up to this new ceiling that we have for ourselves. Making more money doesn’t automatically mean that you need to go out and spend more money. I get it. It’s hard

not to want to go out, and celebrate, and spend your new paycheck on something new. And that’s fine. You can totally go out and celebrate.

But we want to be careful we’re not spiraling ourselves into a snowball effect of additional spending. There’s actually a name for this phenomenon because it’s so common. It’s called the Diderot effect. You get a raise and you decide, well, I want to buy a nice new couch. I’ve been wanting a couch for a while. And then the new couch arrives, and it makes those two old chairs next to it look dingy and unworthy. So, you gotta go out and buy two new chairs. And now, how can you not accessorize that room?

Because with the new couch and chairs, there needs a pillow and coffee tables, because the old ones look so yesterday. And now unthinkingly, you’ve just done a complete makeover in a room when the raise you got didn’t really even cover the cost of the pillows on that new couch. But now, you’ve spent way more than you really originally intended.

I like to call this the, when you give a mouse a cookie effect, because it’s like those children’s books. If you buy a mouse a cookie, he’s going to want a glass of milk, and then he wants a straw, and then a napkin, and then a mirror and so on. It just keeps going, and going, and the snowball keeps getting bigger and bigger. So, we really want to be mindful. It’s okay to go out and celebrate, but we just want to keep it in check.

©Productivity Paradox Page 6 of 8

Now, it wouldn’t be a full conversation about finances if we didn’t talk about debt. Because I know debt is something that a lot of people deal with, and getting out of debt can be hard. With the majority of Americans are faced with debt at some point in their lives so, it’s something we all deal with. Here are a few things to consider if you’re trying to get your bank balance out of the red.

Start by tracking your spending and your budgeting. I know that seems really simple, but it’s amazing how many people don’t do this, because it takes time. Many times, our credit cards can get us into trouble, because we don’t realize the damage of our spending actions until it’s too late and the bill is in our hands. But if you’re regularly tracking your spending, maybe doing things like financial Fridays, you’ll be able to see where you could trim some of that fat on your spending.

It will help you find ways to cut back, and establish a budget so you can work on downsizing your debt. If you see, for example, six transactions at the local convenience store and you know it’s because you’re splurging on Slurpees, maybe it’s time you could budget that down and shift that money into saving instead. So that’s just a really quick and easy way. Use those financial Friday’s to your advantage.

The other thing is to start small. Work on paying smaller debts off first, and then you can eliminate one debt at a time, and lower the amount of monthly fees that you’re accumulating. That’s really where we get hit really hard. It’s with all these monthly fees. Then if you close out one credit card or a debt the following month, you can shift those monthly minimums you were paying on that card to another and keep building up.

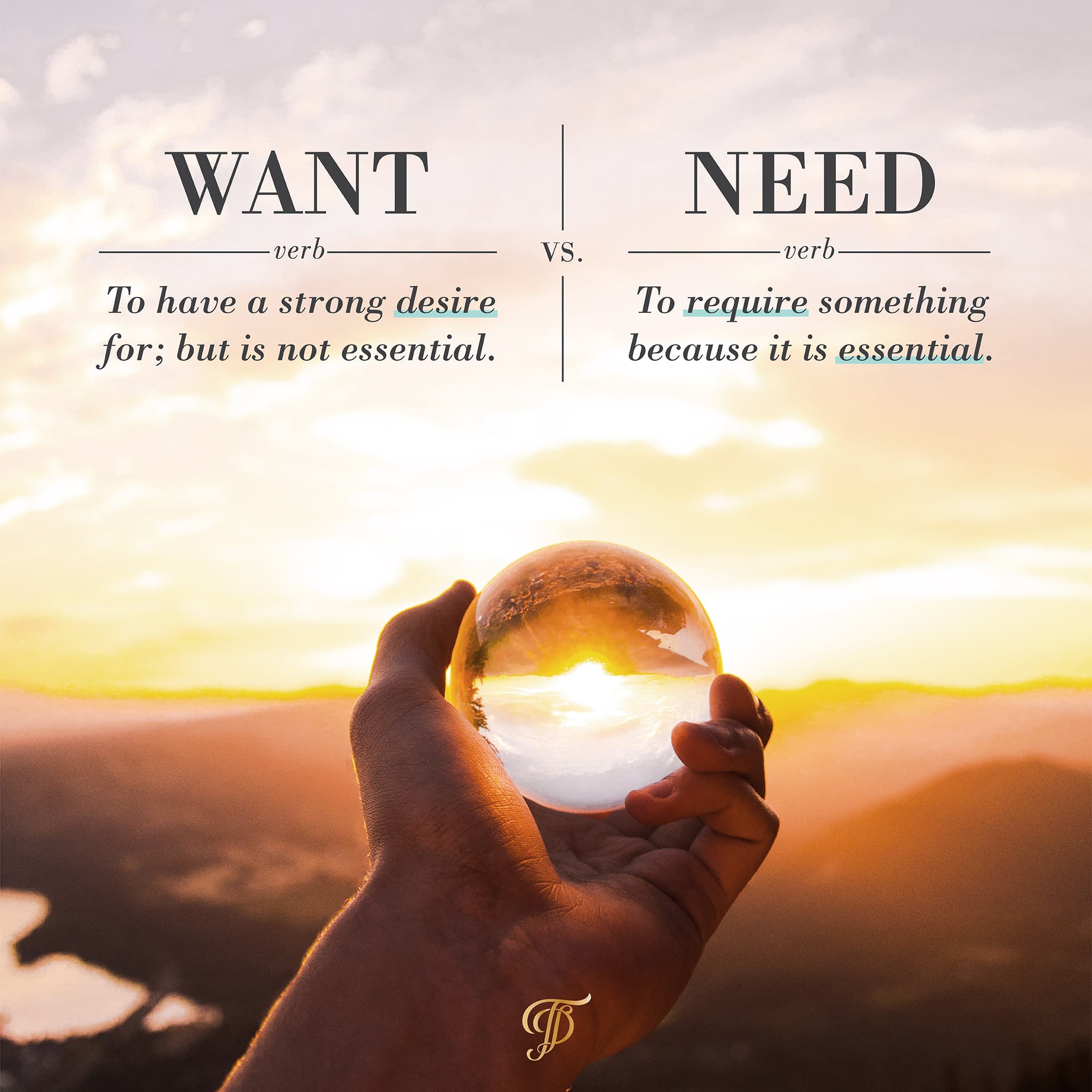

Focus on one card at a time. You want to make sure you’re hitting the minimums for all your cards, but really investing in one to really get that one paid off before you move to the next instead of spreading it out. I want you to also think about want versus need.

We have to shift our mindset, and start thinking in terms of want versus need when it comes to our spending. You need to put gas in the car to get it to work, but do you need that latte every morning? Probably not. It is nice, but it’s a want. And even skipping that latte every other day could mean shifting an extra $15 a week even, to your credit card bill. The little tiny bits really do add up and make a difference.

And my final suggestion, use the cash envelope system. Listen, this system has been around for decades because it works. Go on a credit card diet and pay for things only with cash. You’ll find it’s easier to skip some of the frivolous things when you have to actually pull out physical cash to pay for it. It forces you to pay a little more attention to your spending. It’s a really simple and easy thing to do, but I promise you, it works.

I understand that managing finances can be scary. It can be daunting and really overwhelming. But using some automation, setting up some good habits can help you stay on top of paying your bills, tracking your expenses and avoiding late fees, which is where a lot of us really get hit hard.

With just a few simple shifts to our mindset, we can work towards saving intentionally and downsizing our debt. I hope that today’s episode has given you a few ideas to

©Productivity Paradox Page 7 of 8

help you find some financial freedom. When you feel like you have a good handle on your finances, it really does go far in boosting your confidence and helping you feel a little bit more like the true you we’re talking about all season long.

Now, before I share the next week’s episode, I want to share a review from iTunes. This is from Red Rose 82012, who says, “Goal setting seems to be something on everyone’s to do list. But actually getting them set and then seeing them achieved, that’s another

story. I love the practical tools, and the blend of wisdom, and encouragement to see through and get the dream in your heart a reality. Great podcast for everyone.”

Thank you so much for the beautiful review. If you will send my team an email with your address, I will be handwriting a thank you note and sending that out your way this week.

And speaking of the week to come, what’s up next for our Productivity Paradox? We are going to be talking next week about improve your sleep, and increase your productivity. Another week focused on the new year true you. So, becoming even more productive, even happier through better sleep.

I do want to let you know too, that the video I mentioned earlier on how to organize your kitchen, where I show some of the tips and tricks in my own kitchen, that’s available for you to watch at inkWELLpress.com/youtube. So, be sure to give that a watch.

All right. Until next time, have a beautiful and productive week.

Thanks for listening to Productivity Paradox. To get free access to Tanya’s valuable checklist, five minutes to peak productivity, simply go to inkWELLpress.com/podcast.

{kind=link}

{kind=link}